by Julia Seibert

52 years ago, the future of spaceflight was in NASA’s hands. Today, that fate lies with private companies.

Though the origins of private spaceflight date back to the 1980s, it is in the past decade that its influence became hard to ignore. In a field previously dominated by governmental missions, several private actors carved out a niche for themselves and are now helping create markets of their own – markets that are beginning to eye up the economies of deep space.

In the upcoming article, we will explore the best private spaceflight companies that are driving this transformation, achievement, and challenges faced by private space companies.

What are private spaceflight companies?

Though non-governmental spaceflight companies are often lumped together under the term ‘private sector’, there is an important distinction between privately held companies and those that are publicly traded. The latter are not only subject to stricter regulatory standards, but their public ownership means that any setback can send stocks plummeting. In spaceflight, however, failure is par for the course when it comes to developing new, untested technology. Therefore, while some spaceflight companies are publicly traded – such as Rocket Lab and Virgin Galactic – most are private, bringing in the money from angel investors, venture capitalist funds, or personal savings. They are also not required to publish details on business plans and financial circumstances like their public counterparts.

As opposed to governmental agencies like NASA, which are plagued by politics and thin-spread budgets, private spaceflight companies can pursue lofty ambitions with much more freedom. In fact, companies are already overtaking governmental capabilities and are beginning to look far beyond Earth for their business models, such as planning lunar or Martian colonies or looking for asteroids to mine. Still, the current industry is still very much centered around Earth, and governmental customers continue to play a significant part in shaping the industry. However, as the US – where the commercialization of spaceflight is already more advanced than anywhere else – continues to outsource its space missions, it fuels a healthy, independent commercial sector whose pull might eventually overtake that of governments.

Top Private Spaceflight Companies

1. SpaceX

It is difficult to sum up the private spaceflight industry by mentioning SpaceX, because, to a large extent, SpaceX is the industry. The history of commercial spaceflight can be neatly divided into a time before SpaceX, and a time after it.

The linchpin of its success is its partially reusable Falcon 9 rocket, which it unleashed in the 2010s; no other company has since been able to replicate it. Its boosters makeup over half the manufacturing cost of the rocket, and elegantly landing and reusing these – as well as salvaging the fairing halves – allows SpaceX to offer launches at prices other providers can only dream of. Reusing boosters also helps the company launch at a whirlwind cadence of once every few days. The results speak for themselves: the company accounted for 79% of mass launched to orbit in the second quarter of 2023.

Among its other successes are the Dragon spacecraft, which has ferried astronauts and tourists alike to the ISS, and the Starlink internet constellation, which makes up over half of the active satellites currently in orbit. Next on the company’s to-do list is Starship: a fully reusable monster of a rocket that, as of its first attempted orbital test, became the tallest, most powerful one to ever fly. Though it is still in its early (and explosive) testing stages, the vehicle has the potential to singlehandedly turn the industry on its head by launching humans or hardware to the moon or Mars or deploying entire space stations or satellite constellations at once.

In this context, SpaceX stands as the quintessential private spaceflight company, setting the industry’s standards and pushing its boundaries.

Visit company’s profile page.

Explore more: Top 6 SpaceX’s Goals and Objectives

2. ULA

United Launch Alliance (ULA) was officially created in 2006 as a joint venture between defense giants Lockheed Martin and Boeing’s respective spaceflight branches. As described by Ars Technica, the deal was mediated by the US Department of Defense (DoD) after years of competition and lawsuits between the two companies. Their rockets were too expensive to keep up with the commercial market, dominated by cheaper vehicles from Europe and Russia, so they relied on US defense actors for payload – and competed heavily for those contracts. One particular lawsuit, filed by Lockheed against Boeing, caused officials to worry about losing access to Boeing’s Delta rockets and having to rely on Lockheed’s Atlas and its Russian engines. The solution was to merge the companies into ULA, creating a near-monopoly (and prompting a lawsuit from SpaceX’s Elon Musk).

Though ULA may have been the top dog back in the day, its high prices and old-school technology compared to SpaceX have forced it to reimagine its outlook. As the twilight days of the Delta and Atlas rockets and their respective variants approach, ULA is prepping to debut its new beast, Vulcan, in late 2023. The rocket, while expendable, is estimated by ULA CEO Tory Bruno to cost about US $100 million a launch, only about US $33 million more than Falcon 9’s list price. Vulcan outperforms Falcon by a small margin when launching to Low Earth Orbit (LEO) while featuring a much bigger payload bay, making it a more versatile and competitive option in the evolving private spaceflight landscape.

3. Arianespace

Arianespace is the grandma in the private spaceflight industry: it is the very first commercial launch supplier, founded in 1980. Initially partly owned by the French space agency (CNES), the company had the commercial satellite launch market cornered around the turn of the century, while US companies floundered. It operates several vehicles including the small-lift Vega rocket, certain launches of the Russian Soyuz (though Russia’s invasion of Ukraine brought a swift end to the collaboration), and its namesake Ariane out of the European Space Agency’s (ESA) spaceport in Kourou, French Guiana. The Ariane series in particular has been a resounding success; one of its variants, the Ariane 4, reportedly captured 50% of the global launch market during its 113 successful launches from 1988 to 2003.

However, SpaceX soon ate up much of that market share. To make things worse, as the Ariane 5 was retired in 2023, its successor is far from its debut. The Ariane 6’s development was a rocky road; with SpaceX already posing a threat during the mid-2010s, Arianespace’s CNES shares were bought by a joint venture between Airbus and Safran (later renamed ArianeGroup). The latter became primary shareholders and implemented radical changes made to the vehicle’s design in the name of competitiveness. It seems, however, that these changes cost Europe access to space; the rocket remains in a state of perpetual delay.

Arianespace’s long-standing legacy, coupled with the challenges it currently faces, offers a compelling glimpse into the evolving landscape of the private spaceflight industry.

Visit company’s profile page.

You may also like: Top 10 European Space Companies of 2023

4. Blue Origin

Blue Origin is another private spaceflight company hailing from the early 2000s, but its interests are largely different from its rival, SpaceX. Contrary to the latter, who is looking to build a city on Mars, Blue’s vision entails people living on space stations to improve life on Earth. Since such megastations are still a ways away, Blue’s projects are currently spread across many niches, one of them being spaceflight. Alongside sending tourists to the edge of space in its suborbital New Shepard rocket, the company is developing New Glenn, a heavy-lift partially reusable rocket to rival Starship. The rocket is much delayed and is currently still in the hangar, but first customers are confident in a mid-2024 launch; this would be the first time the company reaches orbit. The BE-4 engines used on this rocket are also part of ULA’s Vulcan.

Despite the delays to its rocket program, Blue has its fingers in many other pies. In collaboration with Sierra Space, the company is planning to build a space station known as Orbital Reef in Earth’s orbit. It is advertised as an ‘orbital business park’ where tourists, businesses, and space agencies alike can set up shop, serving as a potential replacement for the ISS as well as a hub for researchers and companies experimenting with space-based manufacturing. Blue Origin has also been selected by NASA to build a crew lunar lander for the fifth of its Artemis missions. In addition, the company is researching a process known as molten regolith electrolysis – Blue calls it Blue Alchemist – wherein lunar soil is heated and turned into solar cells without the need for Earthly material.

Visit company’s profile page.

Learn more: Blue Origin HLS: everything you need to know

5. Axiom

Axiom Space was founded in 2016 by the former ISS program manager, Michael T. Suffredini, and Kam Ghaffarian, former owner of NASA contractor SGT. The company is building a space station to be used by astronauts tourists, research and manufacturing companies, and those wanting to test out technologies in orbit before sending them into deep space. Upon its planned 2026 launch, the first module of the station will dock to the ISS and stay there until the latter’s deorbiting, after which Axiom Station (now consisting of multiple modules) will function independently.

Axiom currently makes headlines for liaising with SpaceX and NASA to send private astronauts and tourists to the ISS aboard the Dragon spacecraft – for the low, low price of US $55 million each (as of 2021; not including costs of living aboard the ISS). Two such flights have already been completed, with at least two more planned for the relatively near future. Though the service is not exclusive to this demographic, the flights have proven especially popular with non-US countries with a space program but no rocket of their own. In addition to this, Axiom is designing NASA’s lunar suits for the Artemis program.

Visit company’s profile page.

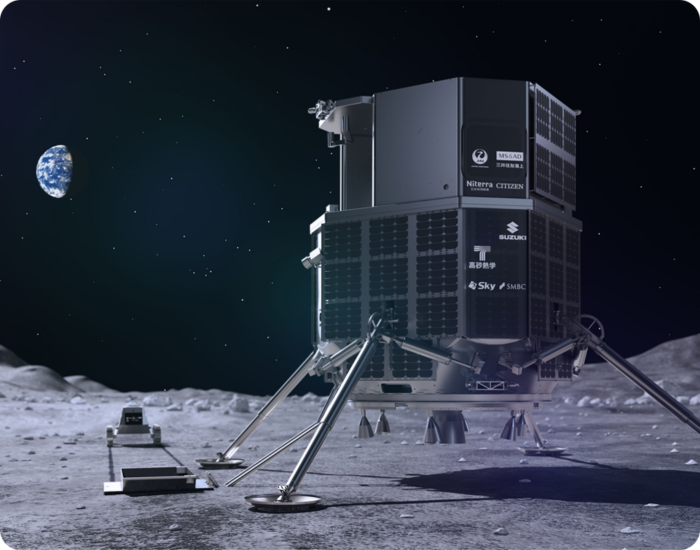

6. ispace

ispace – not to be confused with the Chinese launch startup i-Space – is among a group of companies looking to kickstart a lunar economy. In April 2023, it almost succeeded in performing the first privately funded lunar landing – until the final seconds of descent, when its Hakuto-R lander crashed onto the lunar surface. On its website, the company details an ambitious plan to build a city on the moon known as Moon Valley, which could also serve as a starting point for further exploration. Though ispace has not succeeded in laying the first groundwork, its existence is nevertheless significant as its business model leaves Earth in the dust. This could symbolize the beginnings of a possible shift towards an industry landscape focused on space exploration and colonization, as opposed to other companies mentioned here, whose activities are still centered around Earth.

You may also like:

- Top 15 Best Companies in the World

- Top 8 New Space Documentaries [+3 All-Time Classics]

- The 20 Best Movies about Space to Watch in 2023

Achievements in the Private Spaceflight Industry

One of the biggest achievements of the private spaceflight industry is its very existence. Doing business in space is expensive, risky, and often seen as nonsensical (and sometimes really is), which means that many efforts shrivel and die. However, the miniaturization of technology as well as lowered access barriers to orbit helped companies defy the odds and pursue business in the most hostile of environments. Now, the US is planning its missions around private involvement in lunar exploration and beyond; its cosmic ambitions would be unthinkable without them.

The technology introduced by private spaceflight companies and its impact on the industry is also a significant achievement. Reusable rockets like SpaceX’s are now setting the standard for new vehicles around the world, with companies in the US, as well as China, India, and Europe, working on developing them. This feat has brought about countless new subindustries, some straight out of the pages of sci-fi; space mining, space-based manufacturing, planetary colonization, and many other avenues of business are no longer pipe dreams but are taking their baby steps with private companies. Space tourism, pursued by Blue Origin and Axiom (among others), is also beginning to seem less unimaginable than once imagined. Still, the industry is in its early days, with many potential breakthroughs – such as regular commercial access to the moon – yet to happen. Such a development has the potential to revolutionize the industry in the way regular access to orbit did and the fact that this is even a possibility is an achievement in itself.

Private spaceflight companies are also impacting geopolitics and the role space plays in them. When SpaceX launched its first humans to the ISS in 2020, it was the first crewed launch from US soil since the retirement of the Shuttle almost a decade prior and reestablished the US as a major space power. SpaceX and its competitors can now offer the US government unparalleled access to orbit; Firefly Aerospace, for example, recently deployed a satellite with just 24 hours’ notice for the US Space Force. Other services provided by private companies, such as orbital intelligence and the internet, are also increasingly vital to US defense interests. As a cherry on top, the US government gains these advantages at comparatively bargain prices as companies seek to establish a commercial industry as well, meaning they do much of the work on their own dime.

This unprecedented accessibility of orbit and beyond is reflected in the importance of space-based infrastructure for terrestrial conflict – Ukrainian forces, for example, rely on Starlink internet – as well as the US’s plans to settle on the moon and even Mars, which are at least partially fueled by earthly competition. The control of space granted to the US government through its industry – which US defense entities still have a major hand in shaping – is unnerving to those opposed to its hegemony, such as China. The latter has often accused the US of militarizing space, and the rivalry between the two countries is beginning to spill into orbit as their reliance on the domain grows. A half-baked version of this scenario might have occurred without technology provided by mainly American private companies, but it is this industry that has turned space into the geopolitical hothouse it is today.

Challenges Faced by Private Spaceflight Companies

A hard truth of the space industry is how easy it is to fail, and many companies close up shop following a rocket failure or timelines taking too long. Virgin Orbit, for example, crumbled after its would-be historic rocket launch ended with a dive into the Atlantic Ocean; space mining ventures Deep Space Industries and Planetary Resources were bought up after not following through on ambitious promises to investors.

Even without any disasters, a key challenge in the spaceflight industry is creating a market. Due to the risk and technical difficulties involved, many proposed ideas – such as space mining and manufacturing – have simply never been done before, making it hard to prove the concept’s viability. Just flying a technology demonstration mission can take years of work, highly specific skills, and millions of dollars, which not every investor will be convinced by. This is hard enough in the US, but in more conservative financial climates such as Europe’s, it might be even more difficult to garner support.

Another challenge specific to launch companies is the near-monopoly SpaceX currently has on the Western market. Companies entering the scene must find a way in; while the US government frequently offers small contracts to up-and-comers, it is hard to establish a secure niche that will lure customers away from SpaceX’s low prices. One avenue pursued by several small launch companies is offering transportation to highly specific orbits, which means the payload does less legwork to get to its desired (whereas SpaceX dumps all its payloads out in one go). This is akin to taking a taxi as opposed to a bus. Still, while these small rockets may save the customer payload some fuel, ridiculously low prices like those advertised for Starship when it is operational could nullify that possibility.

Future Prospects

The path ahead in the private spaceflight industry may be marked by challenges and setbacks, but several converging factors are driving a significant trend toward increased involvement of private spaceflight companies in the United States. At the moment, its government is still calling the shots, recruiting companies for its lunar missions and satellite launches. Its purpose, however, is not only to save money; by outsourcing the riskiest, costliest activities, it can get space exploration done on a budget.

There may come a time when commercial interests no longer align with those of government – such as the establishment of sovereign cities on the moon or Mars, which space law forbids – but private spaceflight companies are no longer dependent on their nations for contracts and funding. If and when this happens is hard to tell, since factors vital to such developments (including Starship and the first lunar landings) have not yet come to fruition. What is clear, though, is that at least in the US, there was never any other option; with public opinion of space exploration low but a perceived threat of being overtaken in the field, the only solution is to let the private sector handle it. Right now, the developments in the private spaceflight industry are thrilling – but will that still be the case in another 52 years?

If you found this article to be informative, you can explore more current space news, exclusives, interviews, and podcasts.

Featured image: Liftoff! Atlas V SILENTBARKER/NROL-107. Credit: ULA