Quantum Sensing for PNT Is Shifting From Lab Trials to Operational Deployment Between 2026 and 2036

Insider Insight

- GNSS is no longer treated as a guaranteed signal. Regulators and operators now manage jamming and spoofing as an active condition of flight, reframing PNT resilience as an architectural question, not a procurement one.

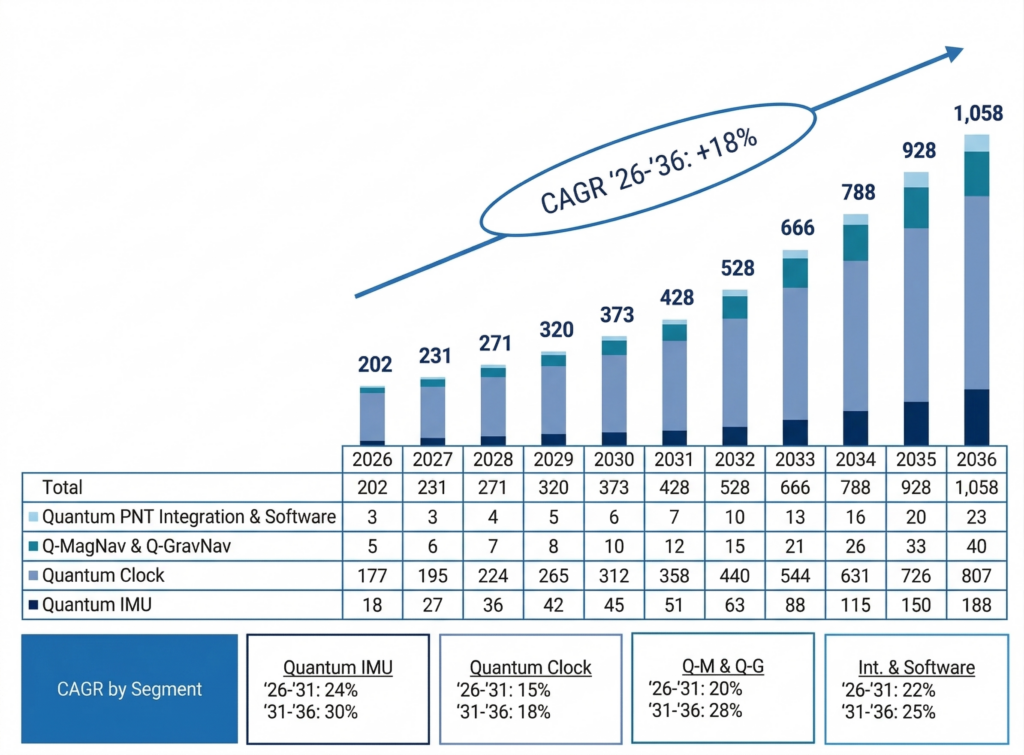

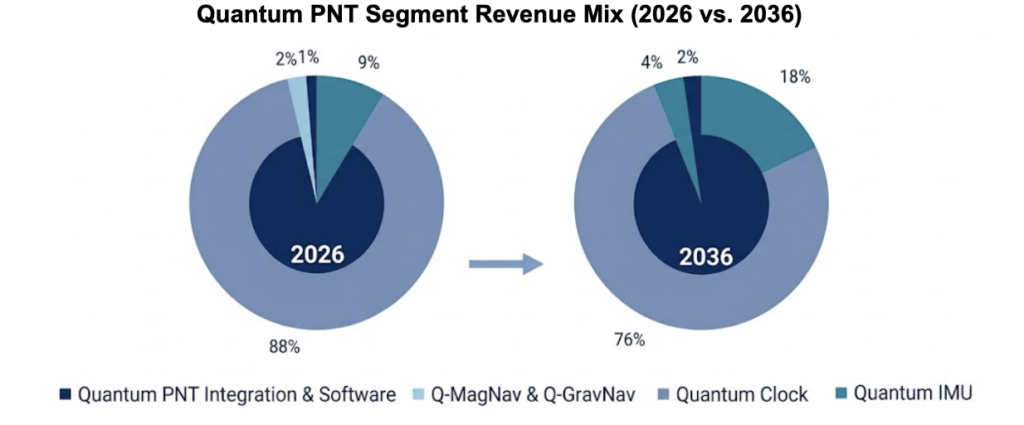

- The near-term market is almost entirely a timing story. Quantum clocks account for ~88% of the 2026 TAM, anchored by sovereign timing trials and defence network deployments, while inertial and environmental layers stay in structured demonstration.

- In contrast, by 2036 the picture is diversification, not replacement.Clocks hold ~76%, quantum IMUs reach ~18% as DARPA RoQS and DIU programmes move toward platform integration, and environmental navigation holds a credible ~4% through magnetic and gravity trials.

Where Quantum Sensing for PNT Fits

Quantum sensing for PNT is moving from laboratory demonstration toward operational deployment. For decades, GNSS (Global Navigation Satellite Systems) has functioned as silent infrastructure — precise, ubiquitous, and largely unquestioned. That assumption is now fading.

However, across contested regions and commercial air corridors, GNSS interference is no longer a theoretical vulnerability; it is an operational reality. Aviation regulators such as the European Union Aviation Safety Agency and industry bodies like the International Air Transport Associatio good night have issued guidance addressing jamming and spoofing exposure. The question is no longer whether GNSS is essential but whether sole reliance on a single externally broadcast signal is sustainable.

Quantum sensing for PNT enters this landscape as physics-based resilience, enabling holdover timing, augmented navigation, and environmental references independent of GNSS.

The analysis below is drawn from Space Insider’s full Quantum PNT Intelligence Report (2026–2036), which maps the market landscape, strategic transition pathways, and vendor dynamics positioning quantum PNT for operational deployment over the next decade.

Quantum PNT Total Addressable Market (2026–2036)

The global Quantum Sensing for PNT market grows from approximately $202M in 2026 to over $1B by 2036. The near-term market is timing-heavy, quantum clocks account for the bulk of early revenue (~88% in 2026), while inertial and environmental navigation grow as assured stacks mature. Full segment-level forecasts, procurement triggers, and vendor benchmarking are modelled in Space Insider’s Quantum PNT Intelligence Report (2026–2036).

Strategic Market Overview

At its core, the strategic case for quantum PNT reflects a simple architectural insight: GNSS signals are fragile at the point of use. Weak space-to-ground transmissions are vulnerable to jamming, spoofing, and interference, creating a single point of failure for both military and critical infrastructure.

What differentiates the current environment is that GNSS degradation is no longer theoretical but increasingly observed and operationally managed. The aviation sector’s evolving risk communications, network synchronization incidents in telecoms, and defense GPS-denial exercises underscore that resilience is no longer optional.

Importantly, quantum sensors, clocks, quantum inertial measurement units (IMUs), and environmental references are not positioned as GNSS replacements. They are positioned as layers that augment and diversify PNT architecture, increasing continuity when satellite signals falter.

Market Map and Segment Composition

Before diving deeper into segments, the ecosystem can be conceptualized around four capability pillars:

- Precision timing (quantum clocks)

- Inertial navigation (quantum IMUs)

- Environmental navigation (magnetic/gravity sensors)

- Integration, software, and fusion

These pillars reflect where investment, programs, and transition pathways are coalescing, not a single dominant “quantum winner.”

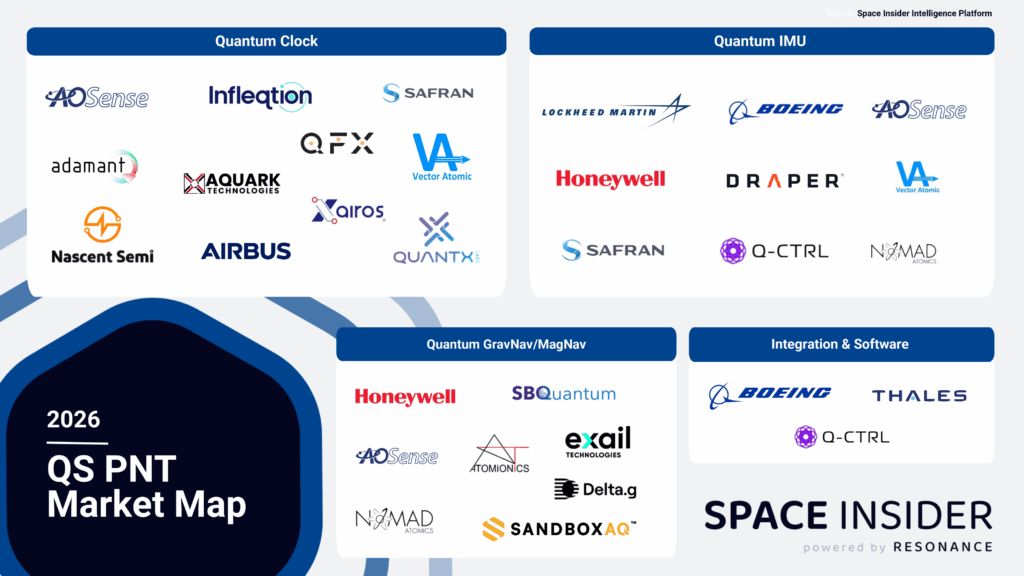

Quantum PNT Vendor Landscape by Capability Pillar

Our QS PNT market map depicts an ecosystem organizing around capability clusters rather than one dominant technology.

- Primes and large defence suppliers are positioned where platform access and procurement alignment matter most.

- Specialist quantum sensor makers concentrate on subsystem performance and deployability.

A smaller integration/software tier addresses fusion and assurance as stacks move toward operational use

Non-exhaustive map drawn from Space Insider's full Quantum PNT Intelligence Report (2026–2036). Clusters show primes, specialist sensor makers, and integration/software tiers aligned to timing, inertial, environmental, and fusion capabilities. The accompanying market map is available for download below.ties..

Segment Composition

In 2026, quantum clocks represent ~88% of the total addressable market (TAM), with quantum IMUs and environmental sensors still largely in testing phases. By 2036, the market shifts toward a more diversified stack: clocks remain dominant (~76%), while quantum IMUs reach ~18%, driven by DARPA RoQS and DIU programs progressing into platform integration, including helicopter, maritime, and space-based testing for GPS-denied navigation.

MagNav and GravNav (~4%) expand through DIU’s Transition of Quantum Sensing (TQS) framework, alongside field validation by SBQuantum and SandboxAQ, and gravity-based maritime trials demonstrating moving-platform feasibility, with software and integration capabilities scaling alongside hardware deployment.

Segment Spotlight: Where Value Emerges

Quantum Clocks — Timing as Anchor

First, precision timing is the most mature and near-term entry point. Quantum clocks address timing resilience needs across defense networks, satellite operations, telecom synchronization, energy grids, and financial infrastructure.

Evidence of momentum includes:

- ESA’s ACES time-transfer validation mission.

- UK sovereign timing trials supported by the National Physical Laboratory.

- AUKUS maritime trials of deployable optical clocks.

- UK Royal Navy tests of Infleqtion’s optical atomic clock aboard HMS Prince of Wales.

- U.S. field trials deploying transportable atomic clocks for infrastructure resilience.

Vendor activity spans specialists and larger aerospace players:

- Infleqtion — U.S. DoD and allied quantum timing contracts.

- Vector Atomic — DARPA and DoD funding for optical clock systems.

- AOSense — U.S. government programs across timing and inertial domains.

- Safran and Airbus — prime engagement in timing architectures.

The clock segment is projected to expand from roughly $177M in 2026 to ~$807M by 2036.

Quantum IMUs — Navigation’s High-Growth Layer

Quantum inertial navigation extends positioning accuracy when GNSS is impaired. The IMU segment scales from roughly $18M (2026) to ~$188M (2036), reflecting strong growth but bounded by platform qualification timelines and SWaP constraints.

Structured defense programs anchor this transition:

- DARPA’s Robust Quantum Sensors (RoQS) program targeting GPS-denied inertial and timing prototypes.

- DIU-backed GPS-denied navigation pathways supporting transition-oriented testing.

- Flight-based and helicopter-based integration trials validating real-world insertion feasibility.

- Spaceborne experiments carrying quantum inertial payloads.

The competitive landscape blends primes and specialist sensor developers:

- Honeywell — leveraging its inertial navigation portfolio and participating in quantum sensing R&D efforts.

- Lockheed Martin — involved in quantum-enabled navigation prototypes and defense transition programs.

- Draper — advancing high-performance inertial navigation research.

- Q-CTRL — developing control and sensor-fusion capabilities applicable to quantum inertial systems.

- Nomad Atomics — emerging cold-atom inertial solutions.

- Boeing — partnered with AOSense to evaluate and test quantum inertial technologies within assured PNT integration frameworks, aligning sensor development with platform-level navigation requirements.

Meanwhile, near-term adoption remains hybrid. Cold-atom accelerometers and gyroscopes are positioned to augment tactical-grade inertial systems by improving bias stability and extending GNSS holdover. The gating factors are ruggedization, SWaP reduction, and certification, not laboratory precision.

Environmental Navigation — Passive Mapping

Magnetic and gravity navigation use environmental anomaly references rather than signals.

Though smaller in TAM, from roughly $5M (2026) to ~$40M (2036), this layer offers passive updates in GNSS-contested conditions.

Transition intent shows in DIU magnetic navigation selections and sea trials validating feasibility.

Vendors include:

- SBQuantum — magnetic navigation demonstrations.

- Delta.g — gravity-enabled navigation development.

- Atomionics — environmental sensing.

- Exail Technologies and SandboxAQ, emerging environmental navigation stacks.

Environmental layers remain trial-driven, limited by mapping infrastructure and data fusion maturity.

System Integration & Fusion — The Foundation of Assured Navigation

Integration and software, forecasted to grow from roughly $3M to $23M (2036) — are structurally essential. Calibration, drift/bias management, integrity monitoring, and AI/ML-enabled fusion convert precision sensors into assured navigation stacks.

Integration clusters include:

- Boeing — platform assurance.

- Thales — fusion and systems integration.

- Q-CTRL — AI-enabled control and fusion tools.

None dominates outright; value accrues where sensor performance meets platform certification.

Strategic Outlook: A Three-Phase Inflection Toward 2035

The transition to operational quantum PNT is best understood as three structured phases, not a sudden commercial breakthrough.

Phase I (2026–2028) — Demonstration Consolidation

Clock and timing deployments accelerate under sovereign timing initiatives and defense trials. Inertial and environmental sensors continue in structured demonstrations rather than broad procurement.

Phase II (2028–2032) — Limited Operational Insertion

Quantum clocks embed in high-value nodes (defense networks, satellite timing backbones). Hybrid GNSS + quantum inertial stacks emerge in defense platforms. SWaP improvements and integration maturity determine insertability.

Phase III (2032–2035) — System-of-Systems Scaling

Architectures envisioned by frameworks such as ESA’s NAVAC PNT Vision 2035 materialize: GNSS complemented by terrestrial timing networks, inertial augmentation, and selective environmental navigation layers. Adoption remains in mission-critical and sovereign domains rather than consumer scales.

Ultimately, the payoff by 2036, a ~$1B+ market, reflects cumulative, disciplined procurement and integration maturity

Quantum sensing for PNT is not a replacement for GNSS, it is a structural diversification of sovereign and mission-critical architectures.