Insider Brief:

- ISAM/ISOM is shifting from experimental demonstrations to foundational infrastructure, driven by the surge from 10,762 active satellites in 2025 to nearly 69,000 by 2035.

- The market will grow from $138M in 2025 to more than $1B by 2035, diversifying from mobility services into refueling, debris removal, assembly, and manufacturing.

- Governments, operators, and investors are adopting ISAM/ISOM to ensure security, extend asset lifetimes, meet regulatory requirements, and capture new revenue streams.

- Reach out to us at [email protected] to access the full ISAM/ISOM Market Intelligence Report, including segment-level forecasts, competitive landscape analysis, and adoption pathways.

Twenty years ago, repairing or refueling a satellite in orbit was reserved for NASA experiments and DARPA concept papers. Today, in-space servicing, assembly, and manufacturing (ISAM), together with in-space operations and maintenance (ISOM), is becoming foundational. With active satellites projected to surge from 10,762 in 2025 to nearly 69,000 by 2035, congestion, costs, and sustainability challenges are forcing a shift from disposable assets toward modular, serviceable, and persistent orbital infrastructure.

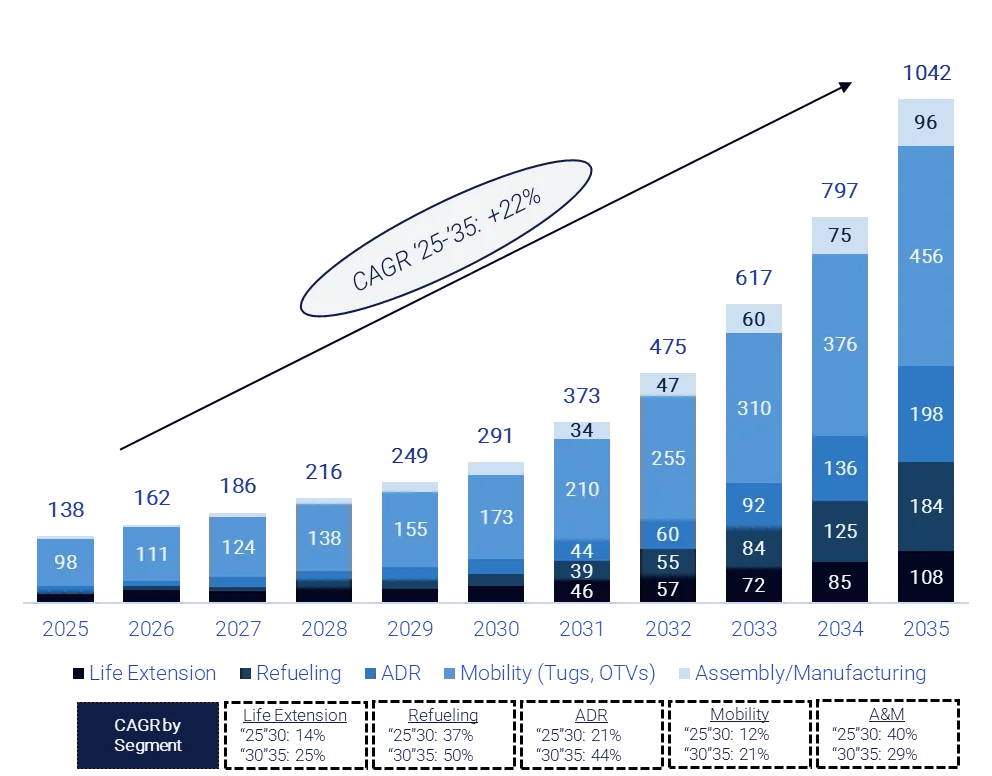

According to Space Insider’s latest ISAM/ISOM Market Intelligence Report, the market will expand from $138M in 2025 to $291M by 2030 (16% CAGR), before accelerating to more than $1B by 2035 (29% CAGR). This trajectory reflects a sector crossing its inflection point from isolated tech demos to sustained commercial services. Published reports often forecast multi-billion-dollar opportunities for ISAM/ISOM by 2030, with on-orbit servicing projected above $5B and broader markets reaching over $20B. Our model applies a hybrid top-down and bottom-up approach: anchoring to credible forecasts but constraining growth with observed contract values, price signals, and adoption pathways.

Why Is Market Demand for ISAM and ISOM Scaling Now

The overall growth goes beyond the inevitable cycle of new technologies maturing. It reflects systemic pressures that make ISAM/ISOM unavoidable. Understanding these drivers is necessary to understand why adoption is accelerating now rather than later.

- Satellite proliferation is creating untenable congestion. Without debris removal and mobility services, collision risk becomes systemic.

- High-value assets in GEO drive demand for life extension and refueling, deferring $300–500M replacement costs per satellite.

- Defense imperatives require maneuverability and inspection capabilities as space becomes a contested domain.

- Heavy-lift vehicles like Starship and New Glenn lower the cost barrier for depots, robotic platforms, and modular assembly.

- Regulators and insurers are tightening ESG requirements around debris mitigation, fueling adoption of ISAM capabilities.

Together, these pressures are influencing procurement strategies for governments, operators, and investors and making ISAM/ISOM essential infrastructure. As these pressures mount, the composition of the ISAM/ISOM market is beginning to evolve. What is today a mobility-dominated sector will likely diversify into a multi-service ecosystem over the next decade, with refueling and ADR emerging as the new growth engines.

How Is the ISAM and ISOM Market Shifting from Mobility to a Service Ecosystem

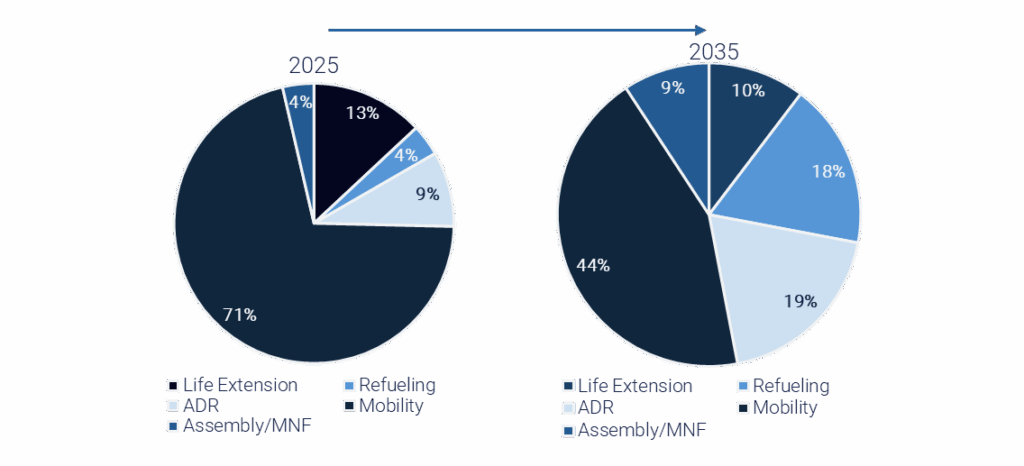

Today, orbital mobility dominates, accounting for 71% of the market as OTVs and space tugs provide the only proven commercial services. But by 2035, the market will look very different. Mobility’s share is expected to fall to 44%, not because it shrinks but because other services expand more rapidly.

ISAM/ISOM Market Share by Segment, 2025 vs. 2035

Refueling, just 4% of the market in 2025, rises to 18% by 2035 as standardized depots and RAFTI-compatible interfaces make “fuel-as-a-service” a recurring model. ADR more than doubles to 19%, moving from government pilots to compliance-driven mandates. Assembly and manufacturing, still niche today, captures 9% by 2035 with deployable structures and in-space 3D printing. Life extension slips to 10% share, as modular spacecraft reduce dependence on external servicing

ISAM/ISOM Market Forecast by Segment, 2025–2035 in Millions. Note: Data labels in the bar chart are shown for all major segments from 2031 onward.

Overall, what emerges is a diversified ecosystem, where mobility remains vital but is no longer the sole driver of growth.

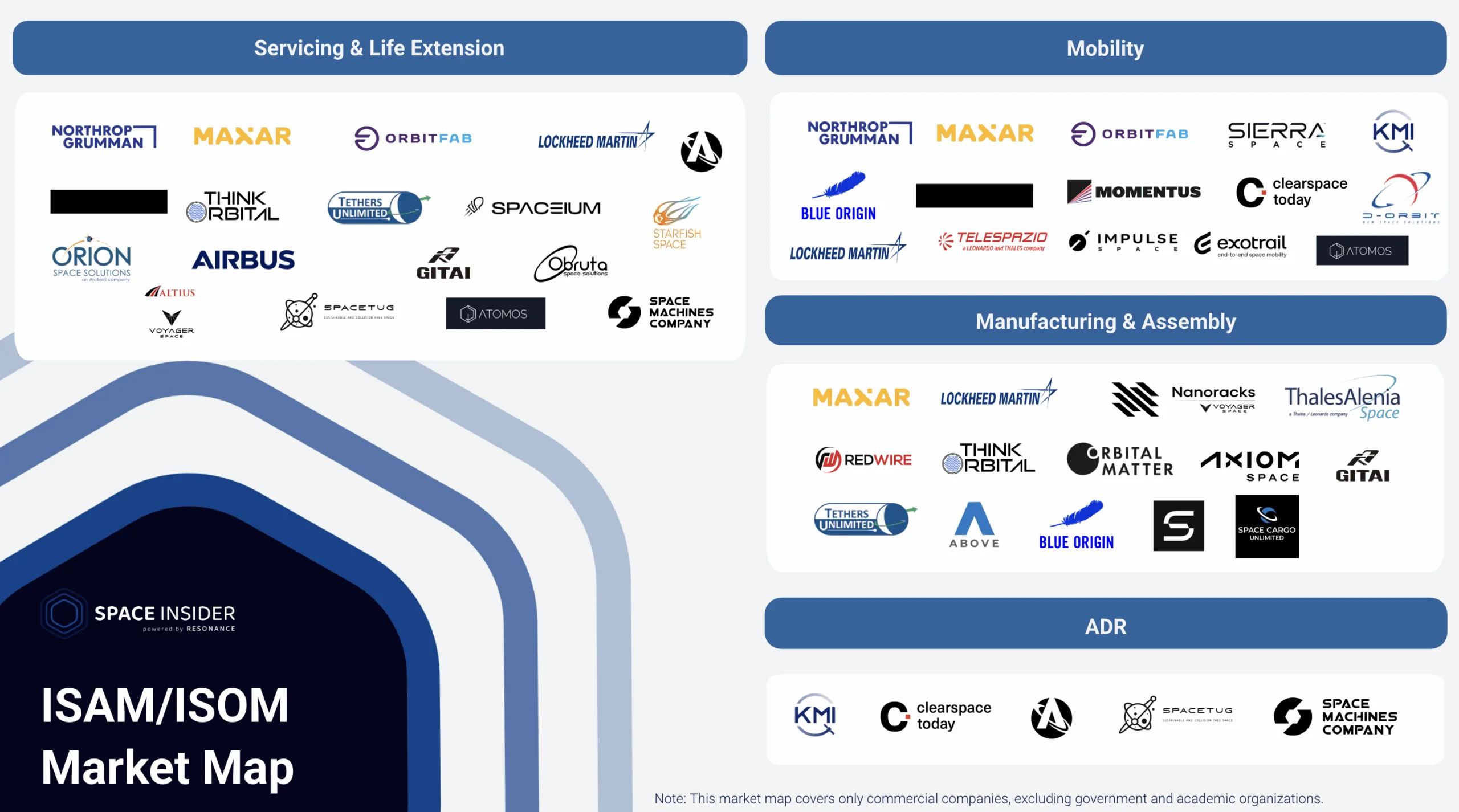

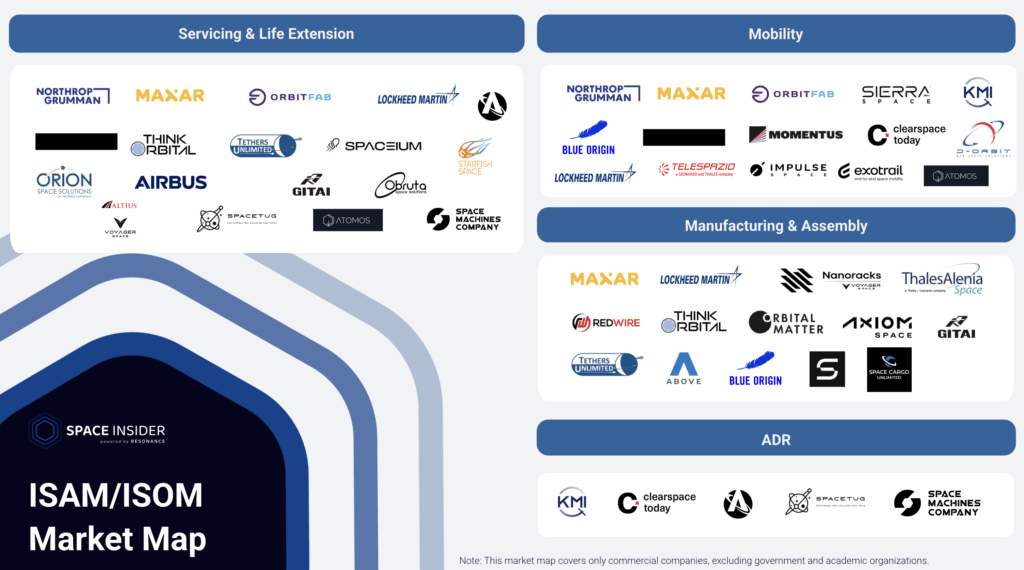

What Does the Competitive Landscape Look Like Across Primes, Startups, and Public–Private Programs

The ISAM/ISOM market can be defined by a dual track of established aerospace primes and agile new entrants. Northrop Grumman, Lockheed Martin, Airbus, and Thales Alenia Space are anchoring defense-heavy missions and GEO servicing programs. Meanwhile, startups like Astroscale (ADR), Orbit Fab (refueling), Starfish Space (servicing), and ThinkOrbital (assembly) are leaning into specialized niches.

Living in both of these worlds are public–private pilots such as ESA’s ClearSpace-1, DARPA’s RSGS, and the U.S. Space Force’s Tetra-5 program, which are accelerating adoption by de-risking early capabilities

This competitive mix reflects the strategic stakes. At one end, governments and primes are focused on orbital resilience and compliance with emerging regulatory mandates. At the other end, commercial players are driving momentum toward recurring, service-based models that could redefine the economics of operating in space.

Yet even with market pull and new entrants, ISAM/ISOM’s trajectory will ultimately be determined by enabling technologies. Adoption will scale only as fast as robotics, autonomy, and standardization allow.

ISAM/ISOM Competitive Market Map

Which Technology Transitions Define the Next Phase of ISAM and ISOM

The move from demonstration missions to a sustainable ISAM/ISOM economy depends on more than market demand; it also requires the readiness of specific enabling technologies. Each capability represents a threshold where, if it matures, the market expands; if it stalls, adoption bottlenecks follow.

- Robotics & Manipulators are the most visible enablers. Early servicing relied on purpose-built robotic arms designed for tightly scripted tasks. The next phase requires dexterous, multi-purpose systems capable of handling uncooperative targets, conducting complex repairs, and adapting in real time to anomalies. Think of the shift as moving from factory-floor machines to the equivalent of orbital “mechanics” with fine motor control and decision-making support.

- Standardized Refueling Interfaces are essential for making propellant transfer scalable. Orbit Fab’s RAFTI standard is already gaining traction, but until common interfaces are widely adopted, refueling will remain a patchwork of bespoke solutions. Standardization turns refueling into a repeatable service model, leading to “fuel-as-a-service” economics and lowering barriers for both operators and insurers.

- Autonomous Rendezvous and Docking (RPO) is equally critical. Current operations often depend on cooperative clients equipped with docking fixtures or pre-planned trajectories. But the majority of satellites in orbit are not designed for servicing. The future of ISAM/ISOM depends on vehicles that can reliably identify, approach, and capture targets without active collaboration, an autonomy challenge that must effetively harmonize computer vision, guidance systems, and failsafe collision-avoidance protocols.

- In-Space Manufacturing is further out on the horizon, but its implications are profound. Moving from experimental 3D-printed components aboard the ISS to large-scale trusses, habitats, or solar arrays manufactured in orbit will fundamentally change spacecraft design. Instead of launching fragile, foldable structures from Earth, operators will be able to construct resilient, modular systems directly in space, optimized for orbital conditions rather than launch constraints.

- Finally, AI and Autonomy implicate every domain. From adaptive decision-making for anomaly response to long-duration autonomy during months-long servicing or manufacturing operations, artificial intelligence will support ISAM/ISOM in scaling beyond human-in-the-loop constraints. Without AI, servicing remains labor-intensive and limited to highly controlled scenarios. With it, fleets of orbital vehicles could operate semi-independently, coordinating tasks across congested orbital shells.

Taken together, these technology transitions define the conditions for success. Robotics, RPO, refueling standards, in-space manufacturing, and AI are not incremental upgrades, but they are the difference between ISAM/ISOM remaining a niche solution and becoming the baseline infrastructure of the orbital economy.

What Forces Are Driving the Acceleration of ISAM and ISOM Adoption

| Driver | Why It Matters | Impact on ISAM and ISOM Adoption |

|---|---|---|

| Satellite Proliferation | Constellations are expanding from 10,762 active satellites in 2025 to nearly 62,000 by 2035. | Creates congestion and collision risk, making debris removal and mobility services essential. |

| High GEO Asset Value | Drives demand for life extension and refueling as cost-saving alternatives. | Increases need for maneuverability, inspection, and on-orbit responsiveness. |

| Defense Requirements | Space is becoming a contested operational domain. | Increases need for maneuverability, inspection, and on orbit responsiveness. |

| Heavy Lift Launch | Vehicles such as Starship and New Glenn lower deployment costs. | Enables propellant depots, robotic platforms, and modular assembly systems. |

| Regulatory and Insurance Pressure | Debris mitigation and ESG requirements are tightening globally. | Accelerates adoption of ADR and servicing to comply with emerging standards. |

Why Will ISAM and ISOM Become the Defining Infrastructure of the Next Decade

The ISAM/ISOM market is moving beyond its experimental stage and into one of acceleration. What once consisted of isolated demonstrations is evolving into a multi-service ecosystem that integrates mobility, refueling, debris removal, and eventually in-space manufacturing into the baseline architecture of space operations.

For governments, these capabilities are inseparable from national security and orbital resilience. For operators, they represent a financial and operational imperative, extending asset lifetimes, ensuring compliance, and embedding sustainability into long-term business models. For investors, the timing question is especially relevant as the next decade will reveal which segments, refueling and ADR chief among them, become breakout markets with compounding returns.

Ultimately, the organizations that prepare now, before standards and market leaders harden, will determine the pace, cost structures, and rules of the next decade in space operations. Space Insider’s market intelligence and advisory services provide the clarity to prepare ahead of this shift, whether your mandate is security, operational efficiency, or investment return. Learn more about our advisory services and how we can support your strategy by contacting us at [email protected].

Frequently Asked Questions

What are ISAM and ISOM in simple terms?

ISAM is in-space servicing, assembly, and manufacturing. ISOM is in-space operations and maintenance. Together they enable satellites to be repaired, refueled, repositioned, assembled, or manufactured directly in orbit.

Why is the ISAM and ISOM market accelerating now?

Satellite volume, operational risk, launch economics, and regulatory pressure have converged to make servicing and debris mitigation essential.

Which ISAM and ISOM services are expected to dominate growth?

Refueling and ADR are expected to be the fastest-growing segments due to mandates, insurance requirements, and the rise of standardized interfaces.

Who are the current industry leaders in ISAM and ISOM?

Aerospace primes lead defense and GEO servicing while startups like Astroscale and Orbit Fab specialize in emerging commercial categories.

Which technologies must mature for ISAM and ISOM to scale commercially?

Robotics, autonomous RPO, standardized fuel interfaces, AI-supported autonomy, and in-space manufacturing must reach commercial readiness.