Insider Brief:

- Space-based ISR is entering a phase of operational maturity, with 1,602 satellites projected to launch between 2025 and 2030, signaling a shift from rapid expansion to a predictable cadence.

- Electro-Optical systems anchor the market, accounting for nearly half of launches, while RF and IR are the fastest-growing segments, expanding by 15–20% annually as demand increases for real-time detection, missile warning, and tactical intelligence.

- Smallsats dominate new production, representing 87% of launches and driving a dual-speed ecosystem where proliferated low-mass architectures deliver agility, and high-power GEO/MEO spacecraft provide endurance and command-grade capability.

- ISR is evolving into a global operating system for awareness, where industrial predictability, sensor fusion, and data integration define competitiveness. Resonance and Space Insider provide the market intelligence and forecasting tools organizations need to navigate this shift, benchmark suppliers, and identify strategic opportunities in the emerging ISR economy.

Space-based intelligence, surveillance, and reconnaissance (ISR) has reached a turning point where growth is giving way to a consistent rhythm. After years of rapid constellation buildouts, the market is entering a new phase of operational maturity with 1,602 ISR satellites projected to launch between 2025 and 2030. What was once a race to populate orbit is now a predictable launch cadence driven by tranche deliveries, structured replacements, and steady new program rollouts.

Electro-Optical (EO) systems remain foundational to the sector. Radio Frequency (RF) sensing is expanding as a distributed SIGINT mesh, Infrared (IR) is accelerating on missile-warning demand, and Radar (SAR) is transitioning into a stable replacement-led cycle. Together, these layers mark a shift from experimental proliferation to disciplined production.

This analysis, based on Space Insider’s latest market intelligence report, maps global ISR developments across commercial and government spacecraft (excluding China, Russia, Iran, and North Korea) to forecast how sensor-layered intelligence will evolve through the decade.

What Does the New Layered Baseline in Space-Based ISR Look Like

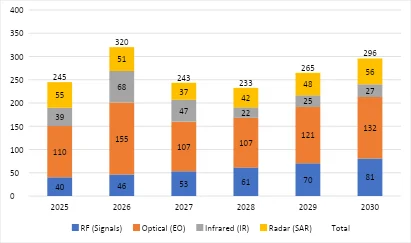

Electro-Optical (EO) systems anchor the ISR landscape, accounting for nearly 46% of launches through 2030. Platforms from Planet Labs and BlackSky sustain EO’s dominance, providing the imagery backbone for defense, climate monitoring, and commercial analytics. Radar (SAR) follows at approximately 18%, transitioning from expansion to programmed replenishment as fleets such as ICEYE, Capella Space, and IRIDE reach operational maturity. Radio Frequency (RF) grows to about 22%, led by HawkEye 360, Unseenlabs, and Spire, reflecting demand for maritime domain awareness, spectrum mapping, and tactical SIGINT. Infrared (IR) rises to 14% as missile-warning architectures like the U.S. SDA Tracking Layer push thermal sensing into the core of defense early-warning systems.

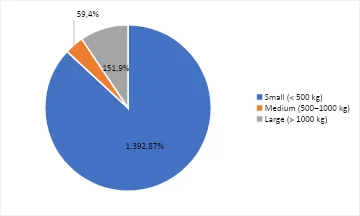

Launch cadence remains uneven with 245 to 320 units annually, reflecting government tranche clustering and commercial refresh cycles. The market skews decisively light: approximately 87% of all launches are Small (<500 kg), demonstrating how miniaturization, standardized buses, and shorter AIT cycles are redefining production scale and responsiveness.

The result is industrial maturity with a supply chain optimised for volume, speed, and interoperability, where small, agile ISR platforms are now the cornerstone of global intelligence infrastructure.

Why Is Space-Based ISR Now Seen as Critical Infrastructure

Space-based ISR has become sovereign infrastructure as a persistent, multi-sensor backbone for deterrence, decision-making, and crisis response. Once a fragmented mix of national and commercial efforts, it is now a coordinated global capability that underpins security, economic resilience, and environmental awareness. Nations increasingly view independent access to sensing architectures as essential to strategic autonomy, ensuring they can detect, attribute, and respond to threats in real time across every orbit.

For operators and investors alike, this maturation changes the nature of competition. Advantage now lies not in satellite count but in operational rhythm, integration, and the ability to fuse data across Electro-Optical (EO), Radio Frequency (RF), Infrared (IR), and Radar (SAR) layers for faster situational awareness. The era of episodic constellation funding is being replaced by programmatic replacement and sensor-mix diversification, creating steadier revenue flows and longer-term manufacturing visibility. Value is concentrating around suppliers that enable standardization, modular upgrades, and scalable production, defining a more predictable and sustainable ISR economy.

What Forces Are Driving the Rise in ISR Launch Volume

The surge in ISR launches is a product of four converging trends that are reshaping how intelligence infrastructure is built, maintained, and renewed.

- Defence Tranches and Sovereign Autonomy: Programs such as the U.S. SDA Tracking Layer and Italy’s IRIDE constellation are setting predictable launch peaks, embedding ISR expansion within national defence frameworks and sustaining production cadence through planned tranches.

- Proliferated Small-Satellite Architectures: A decisive shift toward small-mass spacecraft enables faster iteration and distributed resilience. Standardized buses from AAC Clyde Space and ISISPACE are scaling fleets from dozens to hundreds, which speaks to quantity itself becoming a capability.

- Sensor Layering and Data Fusion: Operators are moving from single-sensor missions to multi-sensor constellations, pairing EO, SAR, and RF data as well as adding IR where strategic missions demand it. This evolution evolves ISR from image capture to real-time intelligence fusion.

- Replacement as Strategy: Fleet refresh is now rhythmic, not reactive. 3–5-year cycles ensure constant coverage and incremental upgrades, converting episodic investment into stable, programmatic industrial demand.

Collectively, they have turned ISR production into a managed industrial cycle, aligning defense demand with commercial efficiency and creating long-term supply predictability.

How Does Each ISR Modality Deliver Value and Where Does It Excel

Each sensing modality within space-based ISR has carved out a distinct operational role, shaped by the type of data it provides and the conditions it can withstand. Together, they form an interdependent system in which no single sensor dominates, but rather each compensates for the limitations of the others to create persistent, all-weather intelligence coverage.

Electro-Optical (EO) satellites remain essential to space-based ISR, delivering the highest launch share and broadest mission coverage across defence, environmental monitoring, and commercial analytics. Constellations such as Planet Labs’ SuperDove and Pelican, BlackSky’s Gen-3, and Copernicus Sentinel-2 form the foundation of persistent global imaging.

Although EO systems depend on daylight and clear skies, their high revisit rates and cross-cueing with SAR and RF constellations enable near-continuous observation. Radar provides the all-weather complement, imaging through cloud, darkness, and smoke for missions that demand uninterrupted visibility. Fleets like ICEYE, Capella Space’s Acadia-class, and Italy’s IRIDE radar segment are expanding high-resolution coverage toward near one-hour regional revisit. The projected moderation in radar launches after 2027 reflects program maturity rather than slowing demand, speaking to radar’s status as a permanent operational fixture.

Radio Frequency (RF) satellites form the tactical mesh of the modern ISR architecture, detecting and geolocating signal emitters in real time. Systems from HawkEye 360, Unseenlabs, and Spire’s Lemur series provide crucial data for maritime awareness, spectrum mapping, and electronic warfare. Compact form factors and rapid refresh cycles make RF the agile, reactive layer that directs optical and radar sensors toward emerging activity.

Infrared (IR) satellites, though fewer in number, deliver outsized strategic value. Architectures such as the U.S. Space Development Agency’s Tracking Layer, the legacy SBIRS, and the in-deployment Next-Gen OPIR enable global missile-launch detection and thermal tracking with near-real-time responsiveness. As dual-band and high-sensitivity sensors mature, IR has shifted from a niche capability to a central pillar of modern defense infrastructure.

Together, these sensing layers illustrate how ISR has evolved from siloed data collection into an integrated network that merges optical, radar, RF, and thermal intelligence to deliver continuous global awareness across every domain.

How Each ISR Sensor Modality Contributes to Mission Needs

| Sensor Type | Primary Role | Growth Trend (2025–2030) | Key Advantages | Example Programs and Operators |

|---|---|---|---|---|

| Electro Optical (EO) | Real-time detection of signal emitters, geolocation, and spectrum mapping | Moderate growth as fleets reach operational density | Strong visual intelligence and broad mission coverage | Planet Labs, BlackSky, Sentinel 2 |

| Radio Frequency (RF) | Near real-time warning and enhanced threat attribution | Expanding at roughly fifteen percent annually | Tactical SIGINT, maritime awareness, and rapid refresh cycles | HawkEye 360, Unseenlabs, Spire |

| Infrared (IR) | Missile launch detection, thermal tracking, and early warning | Fastest growth at about twenty percent annually | Near real time warning and enhanced threat attribution | SDA Tracking Layer, SBIRS, Next Gen OPIR |

| Radar SAR | All weather, day night imaging for surveillance and mapping | Stable growth supported by scheduled replacement cycles | All weather, day and night imaging for surveillance and mapping | ICEYE, Capella Space, IRIDE |

What Do the Launch Numbers Reveal About ISR Growth from 2025 to 2030

Between 2025 and 2030, 1,602 ISR satellites are projected to launch – a clear signal that the market has shifted from rapid expansion to a steady, programmatic production cycle. Launches will peak at 320 in 2026, then stabilise around 250–300 per year as operators move from one-off constellation builds to structured replacements and incremental upgrades. This trajectory represents a broader trend: ISR is now an enduring manufacturing rhythm driven by sensor diversification and value density rather than sheer volume.

How Fast Is Each ISR Sensor Type Growing

ISR growth is redistributing across modalities, reflecting how mission priorities are evolving:

- Electro-Optical (EO): Nearly half of all launches (around 46%), but growth moderates to about 4% annually as constellations like Planet Labs and BlackSky reach operational density.

- Radio Frequency (RF): Expanding at roughly 15% annually, led by HawkEye 360, Unseenlabs, and the U.S. SDA Tracking Layer, as demand for real-time detection and spectrum monitoring accelerates.

- Infrared (IR): Growing fastest at around 20% per year and driven by missile-warning and thermal-tracking architectures such as Next-Gen OPIR.

- Radar (SAR): Launch rates remain stable, anchored by replacement cycles for ICEYE, Capella Space, and IRIDE. This reflects SAR’s maturation into permanent ISR infrastructure, not declining relevance.

Overall, the data demonstrates how ISR is shifting from image capture to multi-domain awareness, where EO, RF, IR, and radar data converge to deliver persistent, all-weather intelligence beyond the limits of optical systems.

How Are Launch Mass and System Architecture Evolving

- Smallsats dominate: Roughly 87% of ISR satellites will weigh under 500 kg, highlighting the rise of proliferated smallsat architectures that favour resilience and rapid deployment.

- Programmatic examples: Initiatives like the Proliferated Warfighter Space Architecture (PWSA) and ICEYE’s standardised bus approach are compressing build cycles from years to months.

- Larger spacecraft resurgence: From 2028 onward, investment increases in high-power GEO and MEO platforms, such as Next-Gen OPIR and European early-warning demonstrators, balancing smallsat agility with command-grade endurance.

ISR is thus evolving into a dual-speed ecosystem where smallsats provide density and responsiveness, while heavy spacecraft supply endurance and power projection.

What Is the Market Outlook for ISR Production Value

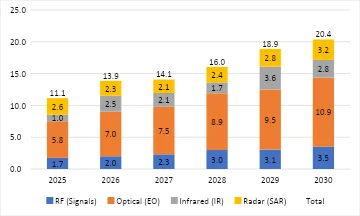

The global ISR spacecraft supply market, representing the cumulative production value of relevant satellites, is projected to grow from $11.1 billion in 2025 to $20.4 billion by 2030, an annual growth rate of roughly 13%.

- RF systems: +15% annual growth, propelled by SDA Tracking Layer and HawkEye 360 procurement.

- IR systems: +22%, supported by U.S. and European early-warning programmes.

- EO systems: Remain the largest contributor (~$50 billion cumulative) through sustained production from Vantor’s WorldView (formerly Maxar Intelligence) and BlackSky Gen-3, though unit value declines as optical systems commoditise.

- SAR systems: Stable production from ICEYE, Capella Space, and IRIDE maintains a strong industrial baseline.

Value creation in ISR is concentrating in high-specification, dual-use, defence-aligned systems. The supply chain is shifting from scaling volume to engineering capability where competitiveness depends on payload sophistication, modular design, and manufacturing throughput rather than satellite count.

Understanding the Next Phase of ISR Growth

What Defines the Next Phase of Space Based ISR Growth

The maturation of space-based ISR signals the emergence of a true operating system for global awareness. As nations, operators, and investors move from episodic expansion to structured cadence, success will depend on understanding where each sensing layer fits within an increasingly interconnected ecosystem. Industrial predictability will reward those who can anticipate the next tranche of demand

For governments and industry leaders, this shift introduces new challenges: balancing sovereign capability with interoperability, aligning procurement timelines with rapid commercial cycles, and extracting actionable intelligence from an expanding flood of multi-sensor data. These are no longer purely technical questions, but strategic, shaping how defense networks, climate monitoring, and commercial services evolve over the decade.

At Resonance, we help organisations navigate this complexity. Through Space Insider’s market intelligence, we map the programs, suppliers, and launch patterns defining the ISR economy and translate global activity into clear signals of opportunity, risk, and strategic positioning. Whether you’re tracking sensor-layer procurement, benchmarking supplier competitiveness, or assessing national industrial capacity, our platform and data products provide the visibility needed to plan confidently in a market where timing, integration, and foresight now define success.

For sensor-level forecasts, supplier mapping, and program-by-program insights, contact [email protected], or explore the full Space-Based ISR Report at spaceinsider.tech.

Frequently Asked Questions

What does it mean that space-based ISR has entered operational maturity?

It means the sector has shifted from rapid constellation buildouts to a predictable launch rhythm where structured replacements, tranche deliveries, and programmatic cadence define production rather than one-time expansion bursts.

Why are Electro Optical, RF, IR and SAR systems growing at different speeds?

Each modality supports different mission needs. EO leads in imagery and analytics, RF grows on maritime awareness and SIGINT demand, IR accelerates due to missile warning, and SAR remains steady because it provides all-weather visibility.

What factors are driving the rise in ISR launch volume?

Launch growth is driven by defence tranche programs, the adoption of proliferated smallsat architectures, multi sensor layering, and the shift to programmatic replacement cycles that maintain consistent coverage and industrial predictability.

Why is ISR becoming a critical national infrastructure?

ISR now serves as a sovereign capability that supports deterrence, crisis response, environmental monitoring, and real time threat detection across multiple orbits which makes it essential for security and economic resilience.

How are sensor types expected to grow between 2025 and 2030?

EO launches moderate as fleets reach density, RF expands at around fifteen percent, IR grows fastest at roughly twenty percent driven by missile warning systems, and SAR remains stable through scheduled replenishment cycles.

How is sensor fusion changing the nature of ISR intelligence?

Sensor fusion combines EO, SAR, RF, and IR data into integrated real-time intelligence streams, which improves situational awareness and enables operators to transition from single image collection to continuous multi-sensor understanding.